How to Avoid Foreclosure in New Jersey

Expert Guidance from Alon Haim – Expert Advisor®

How New Jersey Homeowners Can Avoid Foreclosure

Expert Guidance from Real Estate Advisor Alon Haim

Foreclosure is one of the most stressful situations a homeowner can face. Receiving a foreclosure notice or learning that a Lis Pendens has been filed against a property can create uncertainty and fear about the future.

However, many homeowners in New Jersey are unaware that foreclosure is often not the only option available. With the right information and timely action, there may be several ways to resolve the situation before losing a home.

Homeowners looking to better understand the foreclosure process and their options can find educational resources at www.njstopforeclosure.com, a website dedicated to explaining the New Jersey foreclosure process and possible alternatives that may be available to homeowners.

Real estate professional Alon Haim, Expert Advisor® with eXp Realty, works with homeowners across New Jersey to help them understand the options available when they fall behind on mortgage payments or face foreclosure proceedings.

Understanding the Foreclosure Process in New Jersey

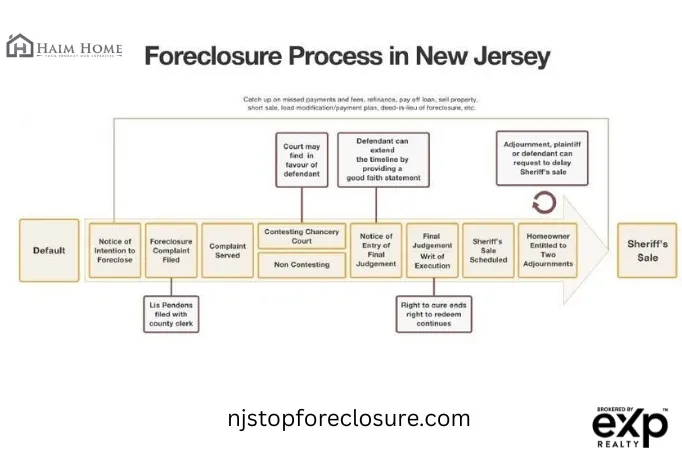

New Jersey is a judicial foreclosure state, meaning foreclosure cases must go through the court system.

The process typically begins after a homeowner falls behind on mortgage payments and the lender issues a Notice of Intent to Foreclose. If the situation is not resolved, the lender may file a foreclosure complaint and record a Lis Pendens, which is a public notice that the property is involved in foreclosure proceedings.

A typical foreclosure timeline in New Jersey may include:

• Mortgage payment default

• Notice of Intent to Foreclose

• Foreclosure complaint filed with the court

• Complaint served to the homeowner

• Lis Pendens filed with the county clerk

• Opportunity to contest the foreclosure in Chancery Court

• Entry of Final Judgment

• Sheriff’s Sale scheduled

• Sheriff’s Sale conducted if no resolution occurs

One important fact many homeowners do not realize is that the foreclosure process in New Jersey is often one of the longest in the United States, frequently taking 12 to 24 months or longer from the first missed payment to a sheriff’s sale.

This extended timeline may provide homeowners with valuable time to explore potential solutions before foreclosure is finalized.

“Many homeowners assume that once foreclosure begins there is nothing they can do,” explains Alon Haim. “In reality, there are often multiple options available depending on the situation and the timing.”

Key Opportunities to Resolve Foreclosure

Even after foreclosure proceedings begin, homeowners may still have opportunities to resolve the situation.

Possible points where solutions may still exist include:

• After missed payments but before legal filings

• After receiving a Notice of Intent to Foreclose

• After the foreclosure complaint is filed

• After a Lis Pendens is recorded

• Before final judgment is entered

• Even after a sheriff’s sale is scheduled in certain circumstances

Understanding the timeline and acting early can significantly increase the number of available options.

Loan Modification or Mortgage Restructuring

For homeowners who want to remain in their homes, one potential option is loan modification, sometimes referred to as mortgage restructuring.

In a loan modification, the lender may adjust the terms of the existing mortgage to make payments more manageable.

This may include:

• lowering the interest rate

• extending the loan term

• adding missed payments to the loan balance

• restructuring the repayment plan

For homeowners experiencing financial hardship, loan modification programs may allow them to stabilize their mortgage and avoid foreclosure while remaining in their home.

Selling the Property Before Foreclosure

Another possible option is selling the property before foreclosure reaches its final stages.

A traditional sale typically works when the value of the property is higher than the remaining mortgage payoff, allowing the loan to be paid in full at closing.

Listing the home on the open market may allow homeowners to resolve their debt and avoid the long-term financial consequences of foreclosure.

Selling earlier in the foreclosure timeline generally provides homeowners with greater control over the outcome.

Short Sales as a Foreclosure Alternative

If the outstanding mortgage balance is higher than the property's market value, a short sale may be an option.

In a short sale, the lender agrees to accept less than the total amount owed in order to allow the property to be sold.

Short sales can be complex transactions, but they may offer several advantages compared with foreclosure.

In many cases, additional debts attached to the property — such as liens, judgments, or secondary mortgages — may be negotiated and resolved as part of the short sale approval process so the sale can move forward.

Each situation is different and depends on the lender, the loan investor, and the overall financial circumstances of the homeowner.

Cash Offers and Faster Sales

Some homeowners facing foreclosure timelines may explore selling their property to cash buyers or institutional investors.

These types of sales may sometimes close faster than traditional home sales, which can be beneficial when foreclosure deadlines are approaching.

Cash transactions often work best for properties that require significant repairs or improvements, or in situations where obtaining traditional mortgage financing for a buyer may be difficult.

Acting Early Is Critical

Timing plays an important role when dealing with foreclosure.

Homeowners who begin exploring their options earlier in the process typically have more potential solutions available.

Waiting too long can significantly reduce available choices and may increase financial consequences.

“The earlier homeowners understand their options, the easier it becomes to develop a strategy that protects their financial future,” explains Alon Haim.

About Alon Haim

Alon Haim is a New Jersey real estate professional with eXp Realty, known as the Expert Advisor®.

Alon Haim helps homeowners and buyers throughout New Jersey with all types of real estate transactions, including traditional home sales, luxury listings, distressed property situations, and complex negotiations.

Known for his elite negotiating skills and strategic advisory approach, Alon Haim works to protect his clients' interests and achieve the best possible outcomes whether they are buying, selling, or navigating challenging financial situations such as pre-foreclosure or short sales.

He serves homeowners across the following counties:

Bergen

Monmouth

Passaic

Essex

Morris

Hudson

Somerset

Middlesex

Warren

Sussex

Ocean

For more information about foreclosure options visit:

To learn more about Alon Haim and real estate services throughout New Jersey, visit:

Phone: (insert phone number)

Email: (insert email address)

Disclaimer: This article is provided for informational purposes only and should not be considered legal or financial advice. Homeowners should consult qualified legal, financial, or housing professionals regarding their individual situation.

Facing Foreclosure in New Jersey?

Request Confidential Guidance

Request a Free Confidential Foreclosure Options Review

Your information is kept strictly confidential. A response is typically provided within 24 hours.

Frequently Asked Questions About Foreclosure in New Jersey

How long does foreclosure take in New Jersey?

New Jersey is a judicial foreclosure state, meaning the foreclosure process goes through the court system. In many cases the process may take 12 to 24 months or longer from the first missed payment to a sheriff’s sale depending on the case and court schedule.

Can I sell my home if foreclosure has already started?

In many cases homeowners may still sell their property after foreclosure proceedings begin, including after a Lis Pendens is filed. Options may include selling the home traditionally if the value exceeds the loan payoff or pursuing a short sale if the loan balance is higher than the market value.

What is a short sale?

A short sale occurs when a lender agrees to accept less than the total mortgage balance in order to allow a property to be sold. In some cases liens or judgments attached to the property may also be negotiated as part of the short sale approval process.

What Happens After a Lis Pendens Is Filed in New Jersey?

When a lender files a foreclosure complaint in New Jersey, a Lis Pendens is typically recorded with the county clerk. This document provides public notice that a foreclosure action has begun against the property.

Even after a Lis Pendens is filed, homeowners may still have options. Depending on the situation, possible solutions may include catching up on missed payments, pursuing a loan modification, negotiating a short sale, or selling the property before a sheriff’s sale occurs.

Understanding the foreclosure timeline and exploring available options early can help homeowners make more informed decisions before the process progresses further.

Homeowners facing foreclosure in New Jersey can request a confidential consultation to review their situation and discuss possible options before a sheriff’s sale.

Alon Haim assists homeowners throughout:

Bergen, Monmouth, Passaic, Essex, Morris, Hudson, Somerset, Middlesex, Warren, Sussex, and Ocean counties.